Save for Your Child’s Future– My daughter will soon be 5 years old and though we have made some investments for her, we realise how it needs more conscious planning now. In another 13 years, my daughter will start college, which considering the rate of inflation is going to be a substantial amount. Many a times, we as parents often overlook how expensive college education can get by the time our kids grow up. Gone are the days when children were encouraged to become doctors or engineers. For children today, the whole world is their oyster and you do not want to be caught napping when the time comes.

It is of utmost importance that you plan well before investing in any of the many avenues available. The first thing to do is know and understand about your goal, in this case your child’s education. This calculator helps you to do your homework and how much amount you are going to need by the time your child is ready for higher education.

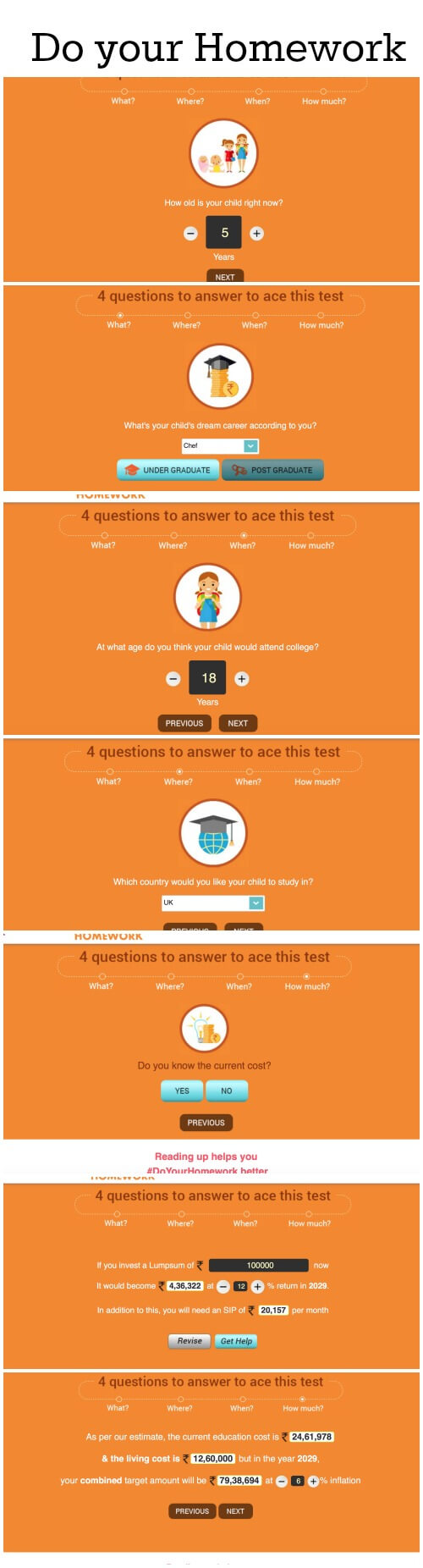

The calculator has 6 steps where in you can choose your child’s current age, preferred profession, the age at which your child will need the amount and the calculator the goes on to give you an estimated amount that you are going to need at that time in future as well as the suggested amount your should invest every month.

Below snapshots will helps you understand it better, it is best to try it yourself.

Now, many of you know that I was a software developer, before I started this blog, but you may not know that I was working for an International Investment bank, which fortunately helped me to understand many financial instruments and their importance.

Today I am going to share with you 5 ways to save for your child’s future.

5 ways to Save for Your Child’s Future

Government Schemes/ PPF/ SSA

These are again very popular ways to save specially for long term goals like children’s education or marriage. These are Government schemes and hence they are relatively safe, although the rate of interest may change overtime.

You can choose Public Provident Fund (PPF) to save for your child. It will give you 8.70% per annum (compounded yearly). You can invest minimum INR. 500/- upto a maximum INR. 1,50,000/- in a financial year. The maturity period is 15 years which can be extended by 5 years. Best part is interest is completely tax free.

If you have a girl child, the newly launched Sukanya Samriddhi Account or SSA is also a good bet as it provides similar benefits and slightly better interest rate (9.2%). You get tax benefits under section 80 C.

Equity/ Mutual Funds/ Shares

According to experts, equity mutual funds are the best way to save for a long-term financial goal.

Mutual funds have professionals managing the funds and distribute the invested amount across multiple stock options thus reducing the risk. SIP to systematic investment plan in mutual funds allow you to invest a fixed amount every month as opposed to a lump sum amount in shares.

The above calculator above gave me an estimate of how much I need to save every month to achieve my goal amount.

Real Estate

This is another popular avenue among Indians. You may invest in real estate and sell when the time comes to support your child’s college education. This however can take time, if you do not find a good buyer at the time when you need the money.

Insurance

It is very important for parents to have adequate life and child insurance to protect their child’s future in case of any mishap. There are numerous child insurance plans available out of which you can choose one that suits your needs best.

Fixed Deposit/ Bonds

This is perhaps the most popular way to invest and save among parents in India. Fixed deposits can be a low risk way to save your money. However, experts believe that since returns, i.e interest from these are lesser than the inflation or the price rise, hence the value of your savings may actually diminish with time.

Hence it is prudent to invest in a variety of options to ensure safety of your investment and your child’s future. But the process must begin with actually knowing what and how much you need to save for which you can use this calculator.

Do let us know how you are saving for your children’s future education. Are you using any of the above mentioned avenues?

Dear Priya,

I always rely on Fixed deposits and for my daughter too, I followed the same. But I would like to know whether LIC policies are fruitful? Also, can NRIs avail of the Government/PPF schemes?

LIC policies are not that great as an investment tools. Experts advise keeping investment and insurance separate.

Unfortunately, NRIs cannot open a new PPF or SSY account.

I have invested in ppf and fixed deposits for my child’s future education and marriage.

Thank you for sharing these amazing tips! We should also consider about safeguarding a child’s future not only in monetary terms but also health wise. Parents should also consider saving their child’s cord blood for the future. The lifestyle that we have plus fatal diseases that we keep hearing about makes it important for every parent to think about how they can help their kids. There are many good players like Cordlife India that provide such services in India and Singapore. Consider factors like the preservation technology, after sales services etc. before making any decision.

i have banked with cordlife india, there are good.